Digital Finance Summit Warsaw 2020: Goodbye Clients, Hello People!

‘Loyalty in the age of disruption’ was the theme of this year’s Digital Finance Summit edition, which took place in late February in Warsaw. The main focus was on the soft aspects of banking like trust, values, impact on customer loyalty and ‘green’ trends.

Sounds insignificant to you? Nothing could be further from the truth. Younger generations pay attention to these matters much more than my peers.

Shift change

Banks can see a new generation change very clearly. Family funds, and sometimes significant fortunes, begin to flow from baby boomers to millennials and their successors, Generation Z, whose values and tastes are radically different from the ideals of their predecessors. Therefore, it is evident that the existing methods of building customer loyalty will soon prove ineffective.

In the UK, banks are already paying cash to their customers for transferring accounts from the competitors. This shows that banks are walking a tightrope in terms of trust, as modern technology companies lure their customers away. So it is obvious that they must adapt to millennials by making the offer more attractive, and changing their communication style. During the summit, Bartłomiej Dajer from Credit Agricole asked the perverse question whether customer loyalty in banking is even possible at all.

Monzo vs Revolut

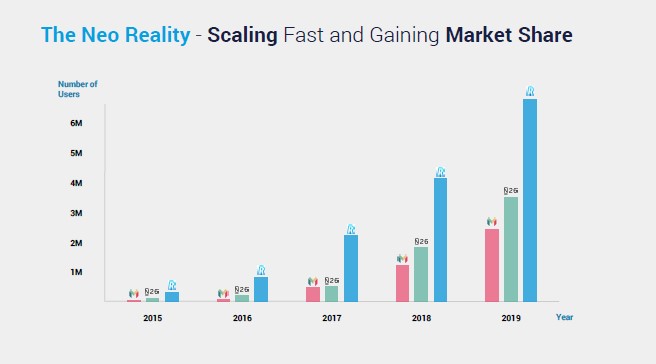

The session that especially caught my attention was Monzo’s. This fintech startup, or rather: a neobank decided to buy a banking license, unlike Revolut. Both companies strive to meet the regulatory requirements, however, Monzo’s ambition is to be perceived as a bank. At the same time, Revolut has no intention to invest in the license, even though it publicly claims full compliance with strict banking regulations regarding customers. And as a matter of fact, the customers have been trusting them.

Monzo and Revolut represent two different approaches, two different business models. Both ‘banks’ are growing very quickly, but it is Revolut that has broken the barrier of 10 million users.

Revolut’s innovative product, a secure card with extremely favourable exchange rates, can convince even the most distrustful customers. Revolut clients are travellers, at least most of them. So, what will happen to Revolut during the coronavirus pandemic? Will people still use their card back in their country? Even if they will, we need to remember that the Revolut business model is based on currency exchange margins, which are calculated upon the client’s travels. The unusual situation we are facing now will undoubtedly affect the company’s revenues. Of course, Revolut is trying to expand in other directions, but will they make it on time?

Speed up the changes

One of the summit’s critical topics was the problem of quick response to changes, or rather the lack of it. Some banks have already noted that they need to focus on this area. Our partner, ING Bank, has abandoned the long lasting RFP process or the waterfall approach. Instead, they switched to the iterative and incremental approach.

An interesting approach was presented by Backbase. Their operating model, developed in the course of projects for Societe Generale or BNP Paribas, cuts the decision making process regarding a project to 6 months. The goal is not to exceed even a year’s quarter. As emphasized by Backbase’s speaker, for banks that use the standard approach, the timeline is approx. 2-3 years! Instead of querying several bidders, Backbase experts recommend scanning the market, setting evaluation criteria and developing a Proof of Concept as soon as possible. Besides, they advise to send RFI not only to companies that first come to mind, but to expand the search systematically. The best bidders in a given industry can be found in the databases of Forrester, Celent, Gartner or IDC. According to Backbase, it is worth talking primarily with industry specialists or at least starting the search with them.

People, not clients

For a very long time, the client-centric paradigm was the primary approach in banking. Everything would start with the customer as all the products were developed for them. During the Digital Finance Summit, it was officially announced that everything starts not with a customer, but with a person.

Banks are entering the role of life advisers, working not through the perspective of products they want to sell, but through the people’s needs. In the new paradigm, the banks are not focused on offering only financial products, but also on supporting people in various life situations. Of course, this wouldn’t work without the numbers (revenue metrics?), and specific products, the range of which expands.

Naturally, banking rhetoric is changing and the industry is walking out of Excel, launching on a journey to communicate with people. It is not about calling the customers to offer them a loan anymore, but about talking to people, understanding their situation and trying to provide support to meet their ongoing needs, without focusing on one product.

This change of tune will no doubt trigger a strong emphasis on personalization. Reaching an individual cannot be based on random trials anymore. Effective operation in a new paradigm includes collecting enough information to know exactly if the bank’s offer matches the needs of the individual. However, personalization requires activating data. In the age of constant changes, only real-life data can be a source of information that would allow reaching people effectively.

CCA Europe has been working on proprietary IT tools for activating financial data for several years. For more information, visit our website, or contact us on the private channel – we are here to help you.