SWIFT transfer? Njet! How does it feel to be on the sidelines of the global economy?

EU’s pivotal decision to disconnect Russian banks from SWIFT over Ukraine casts a stark light on the system’s global economic role. By neglecting to implement ISO 20022 standard, banks might one day find themselves excluded from the mainstream of international money transfer.

Russia’s disconnection from SWIFT transfers as part of the sanctions for its attack on Ukraine was discussed by EU stakeholders for several weeks. For some time, several member states did not support this step. In the end, the Italian finance minister changed his mind. This significantly increased the pressure on the German chancellor, and European values won out over concerns about Russian gas supplies (settled via SWIFT). The decision to disconnect the aggressor’s financial institutions from SWIFT transfer became a reality. Why is this move a decisive one, and why is the SWIFT international payment network so important?

SWIFT as the Orient Express for money

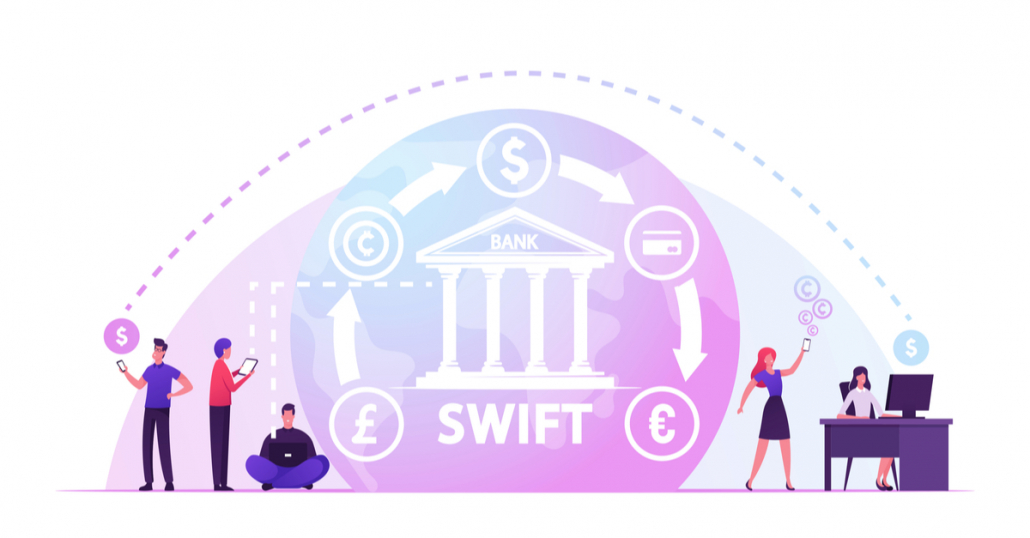

SWIFT, or Society for Worldwide Interbank Financial Telecommunication, is the world’s premier interbank payment settlement system. However, it is not just a mere payment system, as some people think, but a communication system (and definitely not “a WhatsApp for banks”, as I heard one politician put it in an interview recently!).

SWIFT payment system is based on a peer-to-peer relationship between banks. It is not a participant in the transaction, in other words, it is not a “passenger,” but rather a “train” on which data travels from an account at one bank to another. SWIFT allows banks to exchange information necessary to settle a transfer: the sender, the recipient, the amount, type of transaction, etc. Each financial institution that uses the SWIFT payment system is assigned a unique bank identifier code (BIC), which allows it to be identified unanimously. The format of the SWIFT/BIC code includes a 2-letter country code indicating the country where the bank is located. Because this information is described numerically, the payment message can be retrieved and read in all languages as an international bank account number.

The range and standardization of SWIFT network payment messages make the system one of the pillars of international trade. 11,000 banks in more than 200 countries use the network to transfer a total of several trillion dollars annually – in a secure and timely manner. More than 50% of the sum is in US dollars, 30% in euros, and 5% in British pounds.

Any alternative to SWIFT cross border payments?

Banks that oversee SWIFT payments – like the conductor on the train – must follow the rules, including blocking transactions with other banks and sanctioned institutions. Some Russian banks, such as Surgutneftegas, are not yet on the “unwanted passengers” list and can therefore continue to process dollar transactions. One banker quoted by Reuters said that for the time being some of the internal systems of international banks with a presence in Russia could be used, but he believed this was bound to “be a mess.”

Actually, the decision to allow a few Russian banks to remain in the SWIFT payment network is paradoxically better than if all banks were cut off. First, Russia is a major seller of oil and gas in the world. These operations are still allowed and must be accounted for somehow. Second, forward-dated transactions need “an outlet” as they were scheduled months ago and are now awaiting execution. Third, leaving a bottleneck in Russia’s settlements with the world means that banks with the ability to communicate with the rest of the world will sooner or later be crippled by the volume of transactions (similar to a DDoS attack on a website), as en masse customer migrations, both of individuals using foreign transactions and corporations.

It could be some time before individual banks switch to alternative systems for international money transfer, such as TELEX, or implement the indigenous SPFS system, developed after the West threatened to cut Russia off from SWIFT in 2015. And there are also alternatives: systems developed by India (SFMS) or China (CIPS). If, in the meantime, some Russian banks go bankrupt, Godspeed! This will surely provide additional impetus to the eagerly-awaited end of war in Ukraine.

The ISO 20022 clock is ticking

However, there is no denying that SWIFT has not yet had a globally significant alternative. The cutoff of Russian banks from the SWIFT network, or rather its consequences, brings to mind the upcoming massive change that is about to affect this communication standard: the introduction of the ISO 20022 standard and a new SWIFT cross-border transfer format, MX.

The changes will have come into effect in late 2022, with the termination date for the old SWIFT standard set for 2025. Despite appearances, a three-year transition period is not a long time. Preparing legacy systems for ISO 20022 messages requires redefining the entire banking IT infrastructure.

Given the huge number of financial institutions that still use the old messaging format, MT, according to ISO 15022, banks will need to support both the old (MT) and the new (MX) formats during the transition period. To not be left behind in SWIFT communication and thus not to forfeit the possibility of settling cross-border transfers, banks may resort to a temporary solution, a message converter.

Will latecomers be self-excluded from SWIFT?

The exclusion of the world’s eleventh largest economy, which supplies one-sixth of the world’s raw materials, from the SWIFT system is an unprecedented event since the beginning of trade globalization. Western experts estimate that the disconnection from SWIFT could reduce Russia’s GDP by 7%. For many banks around the world, this could also be a demonstration of the consequences that entities that fail to adapt their IT infrastructure in time or ensure an MT/MX message converter will face.

ISO 20022 is an applicable industry standard and banks are required to comply with it. However, we also see it as a huge opportunity for all kinds of financial institutions. Implementation works related to the new standard can be used as a catalyst to strategically leverage the benefits it brings and to create added value. If you need experienced engineers or require consulting support, feel free to contact us.